Cheque and Promissory Note: Cash can be risky and inconvenient to carry when paying for services and goods, yet people still use cash or credit cards in daily life to make purchases; business payments tend to use negotiable instruments as cash may not always be readily available – this article discusses two negotiable documents – cheques and promissory notes – to help explain their respective functions more fully.

Cheque payment method

Cheques are an efficient and secure method of money transfer that we all rely on, from employers paying us via cheques that we deposit into our current accounts to suppliers whom we must pay per invoice due date. Suppliers deposit checks directly in banks that debit our account while crediting their own. Cheques provide an easy and safe payment solution that removes the need for cash they act like documents issued by banks which permit those named on them to claim money listed therein.

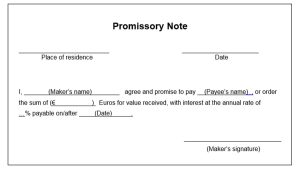

Promissory note

Let’s use an example to better illustrate promissory notes. You can provide security for Matt by issuing him with a document that states you will return his money on a specific date specified on it this document, known as a promissory notice, represents your promise made to Matt about returning it within an established timeline.

Differences Between Cheque and Promissory Note

Here are the main difference between a check and a promissory note:

Nature and Purpose:

- Cheque: A cheque is an instrument for making payments. It’s an instruction written by a bank account holder directing their bank to send an amount to a specific recipient.

- Promissory Note: A promissory note is an official written commitment by one of the parties (maker) to make a payment of a specified amount of money to a different party (payee) at a specific date in the future or upon request.

Parties Involved:

- Cheque: It involves three parties including the Drawer (account owner who is the person who writes the cheque) and the Payee (the bank) and the the Payee (recipient of the cheque).

- Promissory Note: Contains two parties: the Maker (party who makes promises to make payments) and the Payee (party who will receive the payment is made).

Payment Date:

- Cheque: Usually, it is payable upon demand, meaning that it is able to be redeemed right away after it is presented at the banks.

- Promissory Note: This document specifies an exact date for payment that the creator will meet the obligation to pay the beneficiary.

Legal Character:

- Cheque: A cheque can be classified as an order instrument since it directs an institution to make a specific amount to the person who is paying.

- Promissory Note: A promissory note can be described as a promise instrument because it carries the maker’s unrestricted commitment to pay the agreed amount to the recipient.

Transferability:

- Cheque: Highly negotiable and ownership may be transferred by delivery and endorsement.

- Promissory Note: In general, it is less than negotiable, and could require more formal assignments to be transferred.

Purpose and Usage:

- Cheque: Used for payment in commercial transactions.

- Promissory Note: A promissory Note is a popular note used to lend and borrow for purposes, usually in loan agreements or credit transactions.

Default and Dishonor:

- Cheque: Dishonored because of insufficient funds, an account that has been closed or any other reason.

- Promissory Note: A default occurs in the event that the seller does not make the payment promised on the due date specified.

Crossing:

- Cheque: It can be crossed to indicate that it is to be paid at a bank, not through a cash register.

- Promissory Note: Doesn’t contain the notion of crossing.

Guarantor:

- Cheque: Usually does not need a guarantee since it is backed by the balance of the drawer’s account.

- Promissory Note: may require a co-maker or guarantor in particular in the event that the creditworthiness of the maker is in doubt.

Formalities:

- Cheque: Generally, it requires less formalities to issue.

- Promissory Note: may require more specific language and conditions for legal validity.

Presentation:

- Cheque: The person who pays the bill sends the check to the bank in order to pay.

- Promissory Note: A recipient typically waits until the specific date of payment to receive the payment from the manufacturer.

Table:

| Aspect | Cheque | Promissory Note |

|---|---|---|

| Definition | A written order to a bank to pay a specific amount to a person or entity named on the cheque. | A written promise made by one party (the maker) to another party (the payee) to pay a specified amount on a certain date. |

| Parties Involved | Drawer (person issuing the cheque), Drawee (bank), Payee (recipient of the cheque). | Maker (person making the promise), Payee (recipient of the payment). |

| Payment Date | Cheques are generally payable on demand, usually upon presentation to the bank. | Promissory notes specify a fixed payment date in the future. |

| Nature of Instrument | An order instrument, as it directs the bank to pay the specified amount to the payee. | A promise instrument, as it contains the maker’s promise to pay the payee. |

| Legal Nature | Primarily governed by the Negotiable Instruments Act (or similar legislation) in various jurisdictions. | Governed by contract law principles and may not be subject to the same negotiability rules as cheques. |

| Transferability | Cheques are highly negotiable instruments and can be transferred by endorsement and delivery. | Promissory notes are generally less negotiable and may require more formal assignment processes for transfer. |

| Usage | Used for making payments and transactions, often as a substitute for cash. | Used for lending and borrowing purposes, typically in loan agreements and credit transactions. |

| Presentation | The payee presents the cheque to the bank for payment. | The payee typically waits for the specified payment date to receive payment from the maker. |

| Dishonor | A cheque can be dishonored if there are insufficient funds, the drawer’s account is closed, or for other reasons. | A promissory note can be defaulted on if the maker fails to make the promised payment on the specified date. |

| Crossing | Cheques can be crossed, adding an instruction to pay through a bank only. | Promissory notes do not have the concept of crossing. |

| Guarantor | A cheque may not require a guarantor, as it is backed by the drawer’s account balance. | A promissory note may require a guarantor or co-maker, especially in cases where the maker’s creditworthiness is in question. |

| Formalities | Generally less formalities required for issuing a cheque. | Promissory notes may require more specific language and terms to be legally valid. |

| Incomplete Instruments | A post-dated or stale-dated cheque may still be valid and can be cashed at a later date. | Promissory notes may be more dependent on adherence to the specified payment date and terms. |

Similarities Between Cheque and Promissory Note

- Checks and promissory notes have various distinctions and similarities that should be considered when making comparisons between them.

- Both promissory notes and cheques serve to secure payment for specific amounts, thus fulfilling an agreement made between the two parties.

- Checks and promissory notes both represent unconditional promises of payment that cannot be modified due to conditions or contingencies.

- Promissory Notes and cheques are written documents that are legally enforceable and legally bind both parties involved.

- Both promissory notes and cheques bind the payer to pay an agreed-upon amount in full and on time.

- Understanding the distinctions between promissory notes and cheques will enable you to select the ideal instrument for your situation.

When to Use a Cheque or Promissory Note

What type of transaction and parties involved determine whether a check or promissory note would be more suitable;

here are some scenarios when each instrument may be better:

- Use a check when- (payment for goods and services); in business transactions, cheques are often the preferred payment method for goods and services provided to clients.

- Payroll- Employers use checks to pay employees.

- People use cheques as payment for rent, utilities, and credit card bills.

When to Use Promissory Notes:

- Loans: Promissory notes can be used when lending money to people or entities as a legally enforceable obligation to repay their debts.

- Finance Agreements: Promissory Notes are often utilized in financing arrangements pertaining to real estate purchases and investments.

- Investments: When making an investment, promissory notes provide the perfect way to specify terms and repayment schedules.

Before creating or using a promissory note or cheque, always seek legal advice.

Conclusion

Cheques and promissory notes are written documents that promise to pay an amount of money, sharing many similarities such as being written legally binding documents. There are however key distinctions, including their purpose, payee/drawee relationships, endorsements liability versus negotiability; ultimately it depends on your circumstances when choosing either promissory note or cheque for use in transactions.